Multivariate Time Series

Andreas M. Brandmaier

2023-02-17

Source:vignettes/Multivariate.Rmd

Multivariate.RmdThis is a minimal working example that demonstrates how multivariate

time series can be clustered with the pdc package. Note

that pdc can only capture limited information in

multivariate time series and there are likely other approaches that are

better suited to deal with multivariate time series.

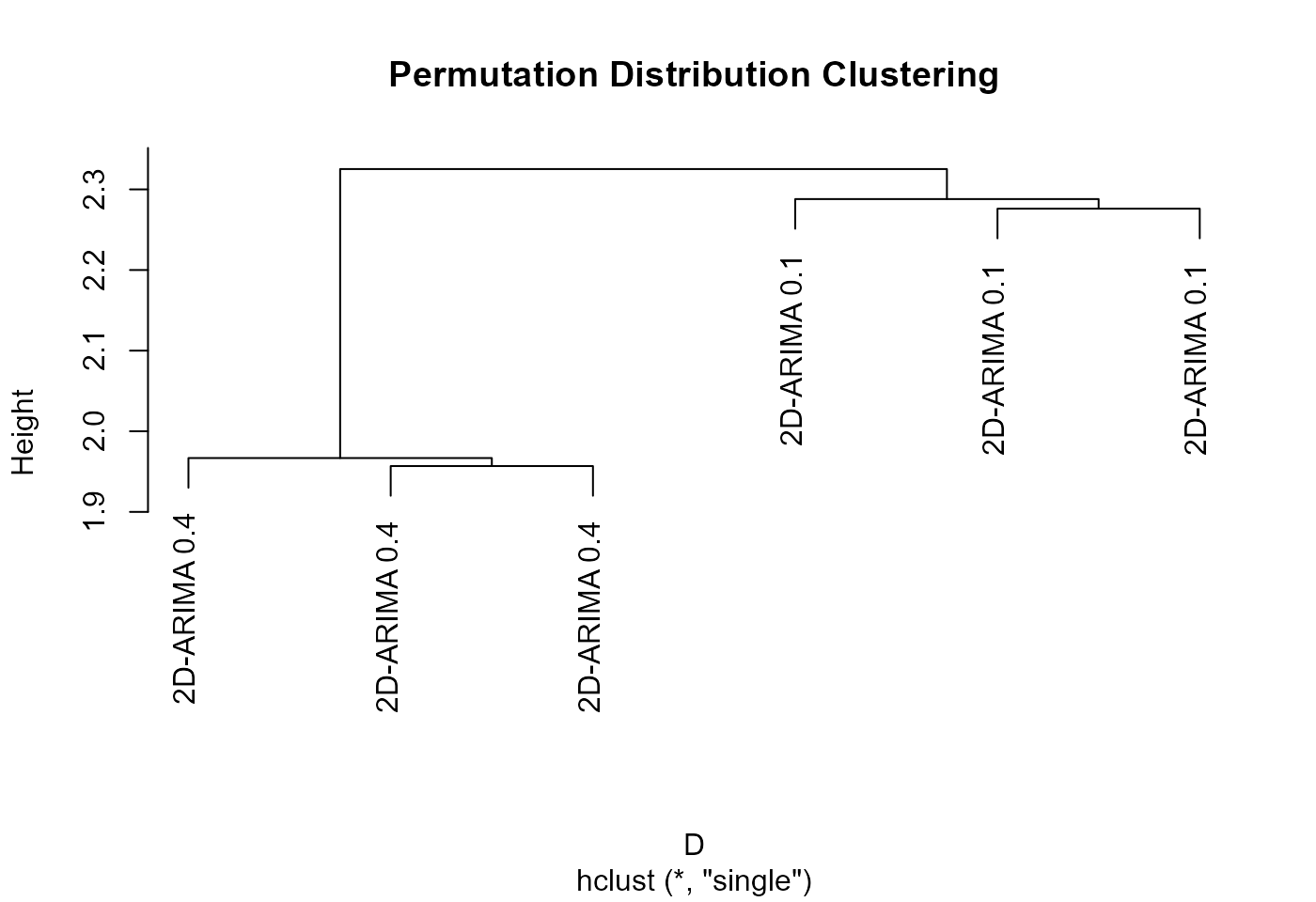

First, we load the package and simulate six two-dimensional time series, each with 5000 observations. The first pair are simulated from an autoregressive process with AR=0.1, the second pair are simulated with AR=0.4.

Note that to this end, data must be arranged in a three-dimensional

array, with the first dimension representing time, the second dimension

identity of the time series, and the third dimension the dimension of

the time series. Here, we create data according to

dim=c(5000,6,2) that is 6 unique time series with each two

channels and 5,000 observed time points.

library(pdc)

set.seed(902101)

ar_params <- rep(c(0.1,0.4), each=3)

X <- array(data = NA, dim=c(5000,6,2))

for (i in 1:dim(X)[2]) {

for (j in 1:dim(X)[3]) {

X[,i,j] <- arima.sim(list(ar=ar_params[i]),n=dim(X)[1])

}

}

labels <- paste("2D-ARIMA ",ar_params,sep="")Run clustering and plot result

result <- pdclust(X, clustering.method = "single")

plot(result,timeseries.as.labels = FALSE, labels = labels)